Recurring Invoice using digital Request for Payment

Using Recurring Invoice using digital Request for Payment

Recurring Invoice using digital Request for Payment and recurring Real-Time instant payments, are defined simply as: Irrevocably collected funds in a Payee bank account and usable immediately by the owner of the account. An upfront on-time 'standing approval' using Recurring Invoice using digital Request for Payment is an instruction or set of instructions a Payer uses to pre-authorize their financial institution to pay future Request for Payments, RfPs without requiring the Payer to review and approve each RfP.

Recurring Invoice using digital Request for Payment and recurring Real-Time instant payments, are defined simply as: Irrevocably collected funds in a Payee bank account and usable immediately by the owner of the account. An upfront on-time 'standing approval' using Recurring Invoice using digital Request for Payment is an instruction or set of instructions a Payer uses to pre-authorize their financial institution to pay future Request for Payments, RfPs without requiring the Payer to review and approve each RfP.

Attributes of Recurring Invoice using digital Request for Payment for your business using instant payments

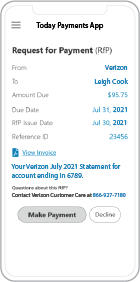

Creating a recurring invoice using a digital Request for Payment (RfP) involves several key elements to ensure accuracy, efficiency, and convenience for both the payer and the payee. Here are the essential elements:

1. Payer Information: Include accurate details about the payer, such as their name, address, contact information, and any relevant identification numbers or account references.

2. Payee Information: Provide detailed information about the payee, including their name, business name (if applicable), address, contact information, and any identification numbers or account references necessary for payment processing.

3. Invoice Details: Clearly outline the invoice details, including the invoice number, issue date, due date, payment terms, and any applicable discounts or late fees. This information helps the payer understand the invoice requirements and payment expectations.

4. Itemized Charges: List all goods or services provided, along with their corresponding quantities, unit prices, and total amounts. This itemization ensures transparency and accuracy in billing, allowing the payer to review the charges and reconcile them with the provided goods or services.

5. Payment Amount: Specify the total amount due for the invoice, including any taxes, fees, or additional charges. Clearly indicate the currency in which the payment should be made to avoid confusion.

6. Payment Instructions: Provide clear instructions on how the payer can make the payment, including accepted payment methods (e.g., bank transfer, credit card, digital wallets), payment deadlines, and any required payment references or codes.

7. Recurring Payment Schedule: Clearly define the recurring payment schedule, including the frequency (e.g., monthly, quarterly, annually), start date, end date (if applicable), and the total number of recurring payments. This information ensures that both parties understand the payment schedule and expectations.

8. Authorization: Include language indicating that the payer authorizes the payee to initiate recurring payments according to the specified schedule. This authorization should be clear and explicit, outlining the terms and conditions of the recurring payment arrangement.

9. Terms and Conditions: Provide comprehensive terms and conditions governing the recurring payment arrangement, including cancellation policies, late payment penalties, dispute resolution procedures, and any other relevant terms. This ensures that both parties are aware of their rights and obligations regarding recurring payments.

10. Compliance and Legal Requirements: Ensure that the recurring invoice complies with all applicable legal and regulatory requirements, including tax laws, consumer protection regulations, and data privacy laws. Adherence to these requirements helps mitigate legal risks and ensures compliance with industry standards.

By incorporating these elements into a recurring invoice using a digital Request for Payment, businesses can streamline the invoicing process, improve payment accuracy, and enhance the overall payment experience for both parties involved.

Creation Recurring Request for Payment

We were years ahead of competitors recognizing the benefits of RequestForPayment.com. We are not a Bank. Our function as a role as an "Accounting System" in Open Banking with Real-TimePayments.com to work with Billers to create the Request for Payment to upload the Biller's Bank online platform. Today Payments' ISO 20022 Payment Initiation (PAIN .013) shows how to implement Create Real-Time Payments Request for Payment File up front delivering a message from the Creditor (Payee) to it's bank. Most banks (FIs) will deliver the message Import and Batch files for their company depositors for both FedNow and Real-Time Payments (RtP). Once uploaded correctly, the Creditor's (Payee's) bank continues through a "Payment Hub", either FedNow or RTP, will be the RtP Hub will be The Clearing House, with messaging to the Debtor's (Payer's) bank.

ACH and both Instant and Real-Time Payments Request for Payment

ISO 20022 XML Message Versions

The versions that

NACHA recommends for the Request for Payment message and the Response to the Request are pain.013 and pain.014

respectively. Version 5 for the RfP messages, which

The Clearing House Real-Time Payments system has implemented, may also be utilized as

there is no material difference in the schemas. Predictability, that the U.S. Federal Reserve, via the

FedNow ® Instant Payments, will also use Request for Payment. The ACH, RTP ® and FedNow ® versions are Credit Push Payments.

Payees ensure the finality of Instant Real-Time

Payments (IRTP) and FedNow using recurring Requests for

Payments (RfP), Payees can implement certain measures:

1.

Confirmation Mechanism:

Implement a confirmation mechanism to ensure that each

payment request is acknowledged and confirmed by the payer

before the payment is initiated. This can include requiring

the payer to provide explicit consent or authorization for

each recurring payment.

2.

Transaction Monitoring:

Continuously monitor the status of recurring payment

requests and transactions in real-time to detect any

anomalies or discrepancies. Promptly investigate and resolve

any issues that arise to ensure the integrity and finality

of payments.

3.

Authentication and

Authorization: Implement strong

authentication and authorization measures to verify the

identity of the payer and ensure that only authorized

payments are processed. This can include multi-factor

authentication, biometric verification, or secure

tokenization techniques.

4.

Payment Reconciliation:

Regularly reconcile payment transactions to ensure that all

authorized payments have been successfully processed and

finalized. This involves comparing transaction records with

payment requests to identify any discrepancies or

unauthorized transactions.

5.

Secure Communication Channels:

Utilize secure communication channels, such as encrypted

messaging protocols or secure APIs, to transmit payment

requests and transaction data between the payee and the

payer. This helps prevent unauthorized access or

interception of sensitive payment information.

6.

Compliance with Regulatory

Standards: Ensure compliance with

relevant regulatory standards and guidelines governing

instant payments and recurring payment transactions. This

includes adhering to data security requirements, fraud

prevention measures, and consumer protection regulations.

By implementing these measures, Payees can enhance

the finality and security of Instant Real-Time Payments

using recurring Requests for Payments, thereby minimizing

the risk of payment disputes, fraud, or unauthorized

transactions.

Each day, thousands of businesses around the country are turning their transactions into profit with real-time payment solutions like ours.

Contact Us for Request For Payment payment processing